Contents

Monetary policy affects the primary asset classes across the board – equities, bonds, cash, real estate, commodities and currencies. Investors should have a basic understanding of monetary policy, as it can have a significant impact on investment portfolios and net worth. To contain the economic fallout of the COVID-19 pandemic, the Federal Reserve took a broad array of actions, including expansionary policy and ‘quantitative easing’ (large-scale buying of bonds and securities). The Fed has been purchasing $120 billion ($80 billion of treasury securities and $40 billion of mortgage-backed securities) every month since March 18, 2020, to support the US economy. Additionally, major elections will be held in 2022 in several emerging market countries amid a polarised political environment, lingering popular discontent and widening economic inequalities.

Suppose large capital outflows from equity markets occur due to the Fed’s tighter monetary policy stance, combined with significant debt repayments and rising international crude oil prices. In that scenario, India’s massive forex reserves may be insufficient to contain downward pressures on the rupee and protect the domestic economy from large outflows. The next section discusses the literature on bank capital channel of monetary policy transmission along with a brief overview of bank capital regulation in India. A basic model has been presented in Section III to explain the role of equity in the credit expansion. Data, methodology and empirical results are set out in Sections IV and V. Concluding observations are discussed in Section VI. The central banks of Australia, Brazil, Canada, Great Britain, New Zealand, South Korea, and Sweden adopted targeting.

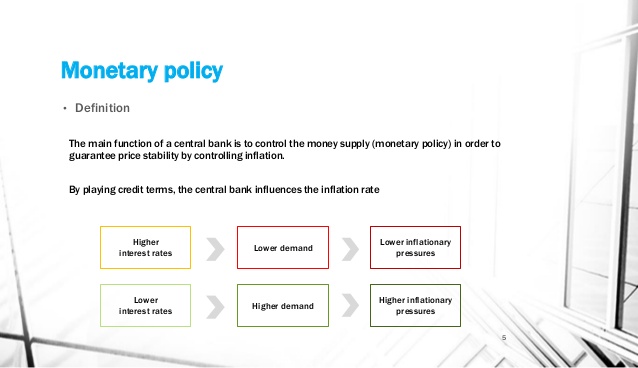

Central banks throughout the world use monetary policy for regulating and managing various variables functioning within the economy. These banks consider using the federal funds rate in order to adjust market factors. When central banks increase the federal funds rate, it results in tightening of the monetary policy. In case, the federal funds rates are reduced, it will result in loosening of the policy.

When the Fed began easing in September 2007, it argued that it was doing so to forestall adverse effects to the economy of falling housing prices. It must do so with information and forecasts that are far from perfect. Tight monetary policy is a central bank’s efforts to contract a growing economy by increasing interest rates, increasing the reserve requirement for banks, and selling U.S.

As discussed in the introduction to the chapter, at the same time the Fed lowered the federal funds rate to close to zero, it mentioned that it intended to pursue additional, nontraditional measures. What the Fed seeks to do is to make firms and consumers want to spend now by using a tool not aimed at reducing the interest rate, since it cannot reduce the interest rate below zero. It thus shifts its focus to the price level and to avoiding expected deflation. Some economists argue that the Fed’s primary goal should be price stability.

The US Fed has committed to maintaining interest rates near zero until inflation averages 2% over time and maximum employment is achieved. In 2022, these economies will face difficulties managing macroeconomic and financial stability in a highly unsettled global economic environment. This year, EMEs will continue to grapple with higher food and energy prices, persistent inflationary pressures and supply chain disruptions. Even if the global economy performs broadly in line with expectations, EMEs will face new challenges this year in bolstering their growth impulses and overcoming financial vulnerabilities. Bernanke has said that his preferred target is the expected rate of increase for the next year in the price index for consumer goods and services, excluding food and energy prices. He has said that his “comfort zone” for expected inflation is between 1% and 2%.

Bonds suffered one of their worst bear markets in 1994, as the Federal Reserve raised its key federal funds rate from 3% at the beginning of the year to 5.5% by year-end. Implementation of the expansionary or contractionary monetary policy depends on the economic scenario. They regulate the money supply in the economy to bring down inflation or accelerate a slowed-down economy. Thetight monetary policy meaningdescribes the contractionary measure adopted by the Federal Reserve to curb the inflation level in the economy. It aims at limiting the money supply in the economy to scale down the purchasing power of the consumers and firms.

In order to keep up with this type of increase in demand for goods, businesses would need to increase production and raise prices if they cannot produce more. When this happens, banks will have less money available to loan out, which increases competition to borrow funds. When the federal funds interest rate moves, so do other market interest rates, such as the prime rate, which can influence interest rates on mortgages, loans, and savings accounts. Different central banks have different tools that they can use to enact tight monetary policy. Tight monetary policy refers to the actions that a central bank takes to limit inflation and an overheating economy.

Identify the macroeconomic targets at which the Fed can aim in managing the economy, and discuss the difficulties inherent in using each of them as a target. The natural consequence of these mounting deficits is a substantial accumulation of government liabilities. Debt held by the public was 35% of GDP in 2007, climbed to 79% of GDP by 2019 and is projected to reach 95% of GDP by 2029.

Similarly, a shift to a contractionary policy in response to an inflationary gap might not affect aggregate demand until after a self-correction process had already closed the gap. The most recent projections expect the annual federal funds rate to steadily climb from 2.3% in 2019 to https://1investing.in/ 2.7% in 2029. Correspondingly, the interest rate on a 10-year Treasury bond is expected to increase from 2.3% to 3.2%. And while the CBO projects Fed profit remittances to the Treasury, it does not provide estimates on how much debt held by the public will be absorbed by Fed banks.

The repo rate is the rate at which RBI lends money to commercial banks. The CRR is percentage of net demand and time liabilities that banks need to park with the central bank. Inflation is the rise in the price level of items, such as groceries or clothes, over time. To minimize or slow down inflation, a central bank could make it more expensive for consumers to spend money and businesses to borrow money by raising interest rates.

Presence of non-performing assets in a bank also weakens monetary policy transmission and lowers the loan growth rate. Low level of CRAR not only hampers bank health but also restricts smooth transmission of monetary policy. Injection of capital by the Government of India in public sector banks is likely to increase the credit flow to the real sector and help in smoother transmission of monetary policy.

According to his argument, when banks extend credit to risky private sector, the risk-weighted assets increase and lead to lower CRAR. Since banks face binding capital constraint, tight monetary policy adversely affects they will fall short of regulatory capital requirement. Instead of lending to the private sector, banks will search for risk-free investment in government bonds.

In the United States, the Federal Reserve is responsible for making monetary policy. The Federal Reserve typically sets the discount and prime interest rates for lending money in the open market. The discount rate is the interest rate banks charge among themselves when lending to each other. The prime rate is the base interest rate charged to consumers for borrowing money. Increasing these interest rates is “tightening” the economy, with several intended effects in personal and business environments. They see an India which is a $3 trillion economy, recording the fastest economic growth in the world, at the cusp of a new credit and earnings growth cycle.

The central bank may follow an easy monetary policy to boost the country’s economic activity. But the same bank may pursue a contractionary or tight money policy if the inflation rises and the government wants to keep it under control. Even if such instruments cannot be fully deployed or remain imperfect, it is unclear whether monetary tightening would pass a cost-benefit test. Such tightening would need to be rather significant to force the restructuring or exit of weak firms. As we have argued, the implied productivity gains would be unclear, and typically small – including for the Eurozone as a whole.

It emphasizes implementing the three prominent contractionary monetary measures, i.e., escalating the open market operations like selling government-issued securities, raising the discount rate, and increasing the reserve requirement. Finally, even if one were to conclude that monetary policy should take account of productivity side-effects, it is quite unclear how one might operationalise such an approach in quantitative terms. That uncertainty would raise the risk of significant volatility in inflation expectations. If sustained, low productivity growth would have profound, adverse implications for progress in global living standards, the sustainability of private and public debts, and the space for macroeconomic policies to respond to future shocks. In conditions of high income inequality, low growth also undermines social cohesion, with adverse political repercussions. The challenge lies in designing an appropriate policy mix depending on the potential macroeconomic and financial risks.

Market analysts predict that the upcoming reduction in asset holdings will be more aggressive, likely totalling $750 billion per year. 1 Capital threshold effect is the optimal adjustment of the portfolio by the banks to avoid meeting additional capital requirement . Macroeconomic policy makers must contend with recognition, implementation, and impact lags. States that people use all available information to make forecasts about future economic activity and the price level, and they adjust their behavior to these forecasts. Explain the three kinds of lags that can influence the effectiveness of monetary policy. The figure below shows debt held by the public as a fraction of GDP, as estimated by the CBO and assuming no interest cost from 2020 onwards.

In this paper, we examine the role of bank capital in monetary policy transmission in India. While higher CRAR helps banks to access funds with lesser cost, it is worthwhile to examine whether these funds ultimately channelize into the credit. In this section, we examine the differential impact of monetary policy to credit supply in the presence of different levels of CRAR. Before studying this hypothesis, we first investigate the relationship between capital and loan growth as shown in Figure 4. On an average, there is a positive association between banks’ loan growth rate and their CRAR.

The Indian economy showed signs of overheating in mid-2007, with inflation rising above 6%. Although the central bank has pursued a tight monetary policy, inflation has recently risen above 7%. Monetary policy refers to the strategies employed by a nation’s central bank with regard to the amount of money circulating in the economy, and what that money is worth.